CVS’s earnings dropped both its stock and Walgreens stock, presenting investors with a possible dip-buying opportunity.

My sentiment analysis on CVS’s recent earnings does not show particularly high pessimism.

Walgreens showed a much more reliable gap for trading or bottom-fishing.

The main reason to buy either of these stocks is to collect dividends.

Looking for a community to discuss ideas with? Exposing Earnings features a chat room of like-minded investors sharing investing ideas and strategies. Get started today »

Both CVS Health (CVS) and Walgreens Boots Alliance (WBA) sold off on the back of CVS’s earnings. One subscriber asked me whether this is a good dip buying opportunity, and if so, which stock is the better buy. Let’s start with my general thoughts on these companies.

Future Outlook: Tough Competition

Without jumping into the specifics of each company, I will say that my future outlook on both of these stocks – as well as any other stock in this sector – is grim. Much like these chain retail pharmacies drove out many small independent operators, we see the competitors of CVS and WBA outperforming in many ways. Companies such as Walmart (WMT) and Costco (COST) run the same business as CVS and WBA but within a larger business.

That WMT and COST offers customers both savings and convenience is a strong competitive advantage. Even if your pharmaceutical purchases at these businesses are not actually cheaper than were you to go through CVS or WBA, the image WMT and COST have crafted for themselves is one of saves. In addition, neither of these companies relies on customers holding the goal of “going to a pharmacy” to snatch their dollars – they only need the customer to be aware of the pharmacy within the retail location to collect afterthought purchases. Some customers likely choose WMT and COST over CVS and WBA because of the convenience. And on that note, the price benchmark setter and king of convenience, Amazon (AMZN), is also a direct competitor with CVS and WBA.

CVS and WBA are one-trick ponies in this regard. But this is merely the macro environment. Few investors consider CVS and WBA as growth stocks. My main point above is that CVS and WBA will have trouble even holding a “value stock” label as pharmaceutical retail businesses become increasingly integrated, diversified, and technological.

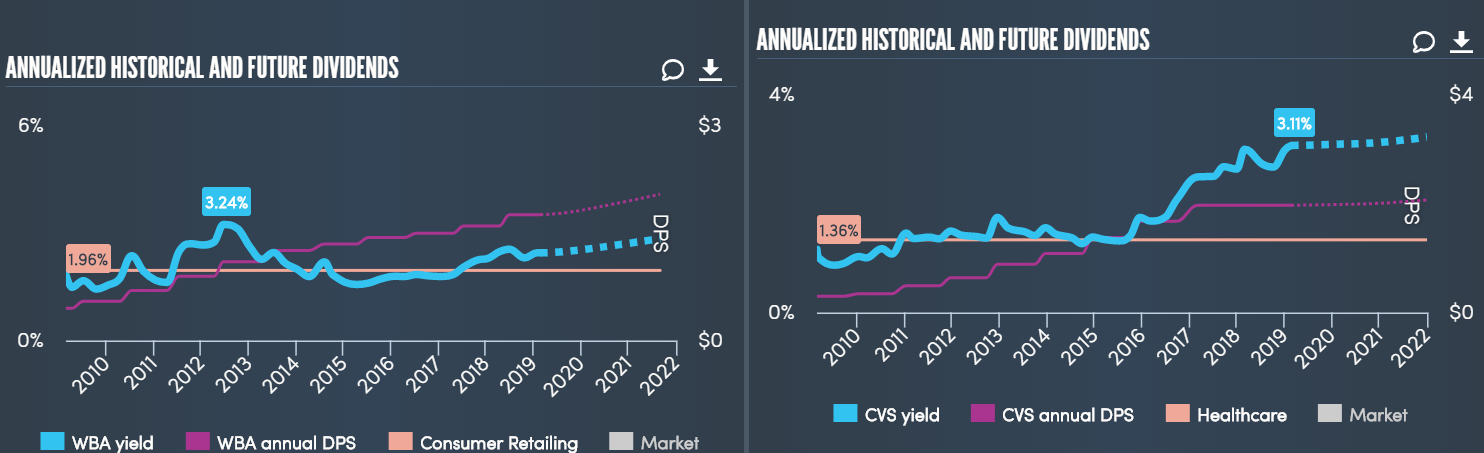

Debt and Dividends

Today, CVS and WBA are most attractive when it comes to their dividends. WBA has been the better of the two over the long term, distributing three times the profit to its investors via dividends versus CVS. In addition, debt levels have kept CVS from growing its dividend in recent years:

(Source: Simply Wall St.)

CVS acquired Aetna, a well-established health insurance company, last year, which cost the company $78 billion. Moving forward, it will possibly benefit from the launch of Aetna-style clinics. However, this is also at the cost of the assumption of Aetna’s debt.

For this reason, debt is more of an issue for CVS than for WBA. Operating cash flow only accounts for 10% of CVS’s total debt. In contrast, WBA’s operating cash flow covers nearly 50% of its debt:

(Source: Simply Wall St.)

Whether this acquisition will help put CVS back on track to raising its dividends or hurt it remains uncertain. However, I believe that when a large, niche business steps into a new sector, it tends to fumble the ball before hitting any significant points. For this acquisition, I say be skeptical until proven otherwise; assume the dividend as is for now.

Still, the benefit in the long term is that CVS can intercept its competitors via leveraging its clinics. The clinics can direct its patients to CVS pharmacies, and thus, can be seen as a strong piece of marketing, if nothing else. Unfortunately, what CVS’s clinic-driven PBM program will become in terms of profitability will remain unknown until later this year.

Was the Earnings Selloff an Overreaction?

However, with CVS’s recent earnings report, we can at least update our outlook on management’s sentiment. Obviously, investors did not respond well to earnings and guidance. But was this an overreaction?

Using the best practices in financial lexical analysis, I have written an algorithm to generate a sentiment score from earnings call transcripts, deriving the general outlook of management. Such sentiment can help predict the future stock price in the coming quarter.

My calculations for Q4 2018, the current earnings report, were optimistic versus CVS’s average sentiment – a 10% increase over the average. However, this was also a 6% drop, quarter to quarter. Overall, these are small changes from the average, and we should not conclude that management is much more optimistic than normal or more pessimistic than last quarter. I believe the drop after earnings is likely an overreaction.

I backtested this, looking for excess gains or losses in CVS (versus the average stock) after news events (including earnings). The company does indeed show a slight pessimistic edge, selling off slightly more than expected on bad news and rallying less than expected on good news. WBA, in contrast, showed average reactions to bad news but, like CVS, showed stunted rallies after good news.

Two Stocks, Two Gaps

Wanting to check whether either of these stocks have a consistent gap pattern, I backtested the gaps on these two stocks after CVS’s earnings. Notably, these gaps are of different types.

The gap we are currently seeing in CVS is rare, with only six instances in the current volatility regime (2012 onward). However, they are reliable short trades. Here is the result of buying the stock after the gap and holding for two days:

(Source: Damon Verial; data from Yahoo Finance)

The sample size is small, but the results for these six data points are consistent over many time periods. After three weeks these gaps stop falling and revert, leading the stock to its post-gap price. To get a more robust understanding, I loosened the definition of this gap; the results are roughly the same over each time period – CVS tends to fall after the gap for a couple weeks before reverting.

WBA’s gap is different and looks much more playable from the perspective of my own gap trading strategies. Yet, it is equally as rare as the gap in CVS. However, unlike CVS’s gap, the backtest shows profitability quickly. Within one week, WBA’s gap reverts and begins to close:

(Source: Damon Verial; data from Yahoo Finance)

I again loosened the definition of this type of gap to find the same results. Here is the one-week profitability with this bootstrapped analysis:

(Source: Damon Verial; data from Yahoo Finance)

That large drawdown is not from this specific type of gap. Recall that CVS’s three-week returns were roughly flat. Here are WBA’s:

(Source: Damon Verial; data from Yahoo Finance)

Hedge Your Bets?

The main question remains: Considering the recent dip, should an investor choose CVS over WBA? With CVS’s future uncertain and with WBA continuing to grow its dividend, WBA might seem like the obvious choice for now.

Of course, you could just hedge your bets and buy both if you are looking to invest in this sector. Alternatively, you could play WBA’s gap. We have already found that WBA reacts better to bad news, which explains the tighter gap. We also know that the gap tends to close at around five days after the gap.

If you were to buy both CVS and WBA, you might want to make the WBA purchase now and the CVS purchase in a couple weeks, as per the gap analysis. My personal advice, though, is to stay away from this sector if you can. Of course, investors hell-bent on reliable dividends still might find these two stocks appealing.

Happy trading.

Exposing Earnings is an earnings trade newsletter (with live chat) that is based on statistics, probability, and backtests. My models are unavailable anywhere else online, as I designed them myself, keeping the code private for Exposing Earnings subscribers and myself. If you want a definitive answer on which way a stock will go on earnings, the probability of the prediction paying off, the risk/reward of the play, and my specific options strategy for the play, click here.